Update on the UK Spring Budget and non-domicile changes

Writing solely about the tax aspects of the recent Spring Budget would result in a very short article indeed—the tax changes are very light in reality. UK Chancellor Philip Hammond was clearly pleasantly surprised by the strength of tax receipts and unexpectedly has a few billion pounds more to play with. Rather than announce tax cuts—which would be typical for a Tory Chancellor to do in these circumstances—he decided to pocket the difference. The entire package of changes announced in the Spring Budget should give rise to a further buffer for him as we head into the unknowable economics of Brexit.

Unfortunately for Philip Hammond, in the days immediately following his Spring Budget announcements, the press was preoccupied with one major tax rise he announced. This would have hit the self-employed hard by increasing their tax bill by 2% from April 2018. Now that Article 50 has been triggered, the Government has got bigger battles to fight in the coming two years so he and Theresa May quickly backtracked on the increase in Class 4 National Insurance rates. The furore was made worse by this particular measure being contrary to the “tax lock” promise the Tories made just two short years ago. It is hard to fathom how the Chancellor and his team forgot this manifesto pledge.

Whilst the Spring Budget was light on tax changes, nevertheless, on 6th April this year, we will be seeing some fundamental changes to the taxation of non-domiciled individuals and also to inheritance tax on property.

CHANGES TO THE “NON-DOM” REGIME

he much trailed overhaul of the taxation regime for non-domiciled individuals is coming into effect in April 2017. Despite this first being outlined in July 2015, we have only just seen the majority of the legislation which has made planning for clients’ individual circumstances extremely difficult.

From 6th April, the concept of “deemed domicile” will extend into the income tax and capital gains tax codes. Domicile is something which could fill many books but the key thing to understand is that it is more adhesive than mere tax residence. It is a question perhaps of “where you belong” as opposed to where you might transitorily be.

Update on the UK Spring Budget (cont’d)

If a non-domiciled individual has been resident in the UK for fifteen out of the last twenty tax years, the new rules will treat them as “deemed domiciled” for all tax purposes. Essentially, they will then be taxed on a worldwide basis whereas previously they would likely have been able to make a claim for the remittance basis of taxation and thus, very broadly, be taxed only on that income and those gains accruing in the UK or where such foreign proceeds are brought to the UK.

Further, anyone born in the UK with a UK “domicile of origin” who returns to the UK from abroad will automatically be unable to avail themselves of the remittance basis of taxation irrespective of any assertion of a “domicile of choice” elsewhere. If they leave the UK again, their alternative domicile of choice can be revived.

In the non-dom suite, there are other aspects we should draw your attention to:

-

- There is an option for foreign assets to be “rebased” for capital gains purposes as of April 2017 (albeit a narrowly drawn relief only available to those becoming deemed domicile on 6th April 2017).

- By becoming deemed domiciled, those individuals with trusts will also lose the income tax, capital gains tax and inheritance tax advantages that they previously enjoyed. However, as long as there are no additions to the trust after 5 April 2017, the individual will only be subject to tax on distributions and the trust will continue to benefit from IHT excluded property status.

- For those who have used the Remittance Basis at some point since 2008/09, they will also be given the opportunity until April 2019 to “cleanse” any mixed funds. The benefit will be that they could segregate the funds, remit the clean capital and leave the untaxed foreign income and gains offshore. Obviously, if they are deemed domiciled, they will be taxed on any further income/gains accruing on those offshore assets but the tax on the unremitted portions can be deferred.

- In other measures affecting trusts, beneficial loans (and loans of artwork) will now attract a charge based on the Official Rate of Interest published by HMRC (presently 3%). Such charges will only be levied where there are pools of income and gains to match with the notional benefit.

CHANGES TO INHERITANCE TAX

As previously announced by the Government, there are a couple of headline Inheritance Tax (“IHT”) changes coming into force in April. The new Residence Nil Rate Band (“RNRB”) plays to the Government’s manifesto commitment to extend the IHT exempt amount to £1m. They have done this in a roundabout way by leaving the individual IHT exempt “nil rate band” (NRB) at £325,000 but phasing in over the next three years will phase in the RNRB which will add an additional £175,000 to that amount (£100,000 from this April). The NRB and the new RNRB bands together of course only amount to £500,000 and this is squared with the £1m commitment by allowing transferability of the bands from the deceased to the surviving spouse. That doesn’t help those who are divorced.

The RNRB will operate where the property (in which the individual has lived at some point) is passed to direct descendants, i.e., children or grandchildren. There are complicated rules compensating those who might have downsized or completely sold their properties to pay, perhaps, for nursing fees and in those circumstances it should still be possible to access the equivalent of the full RNRB.

Bear in mind though that the RNRB gets tapered away once the net estate exceeds £2m so the practical application of this is likely limited.

The biggest IHT change affecting the non-resident community however is that from 6 April, UK residential properties held in structures/wrappers (for example, within a trust or company) will attract IHT unless the company is not “close”. In very simple terms, this means that structures with a broad shareholder base should not be caught.

The benefits of holding a residential property within a company or trust structure have been significantly eroded over the last four years and if anything it is now often very tax-inefficient to opt for ownership in this way. Advice should be taken as, whilst it would often may be the best solution to hold a property personally, where the property is presently held within a wrapper, the tax costs of transferring into the ownership of the individual can be substantial. Unfortunately the UK Government continues to ignore the pressure from the professional community and is refusing to offer some form of “de-enveloping relief” to allow sensible restructuring to take place in a tax neutral environment. Advice should be sought on existing and potential ownership arrangements at the earliest opportunity as there is no “one size fits all” model and whether direct ownership or indirect ownership (through a structure) is the correct answer will depend on individual facts.

CONCLUSION

As painful as these changes are for some individuals, it is an easy political win for the government to make these changes and, lest we forget, we are in unprecedented times of populism and demagoguery.

By 2020, the corporation tax rate will have dropped from 28% to 17% in less than a decade. The UK tax system now appears to be in the last stages of completing its pivot from providing a benign taxing environment for foreign domiciled individuals to a much more business friendly (and private client unfriendly) taxing environment.

About the author

Rawlinson & Hunter (R&H) is an international grouping of professional firms providing full service trust, tax, accounting, wealth preservation and other financial advice to internationally focused, entrepreneurial high net worth individuals and families. Craig Davies is a Partner in the London office of R&H and works with entrepreneurial clients across a wide range of sectors and service lines.

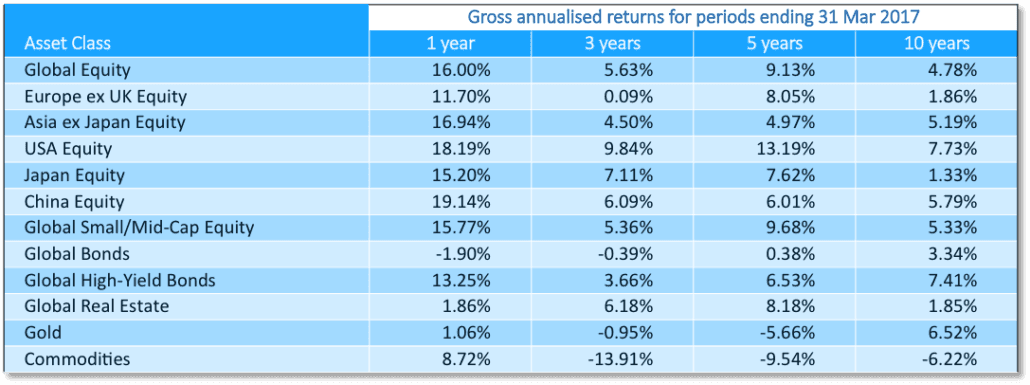

Now you feel it. Now you don’t.

My favourite chart this month below shows a significant disconnect between survey-based indicators like Consumer Confidence and ISM and the “hard data” indicators like Unemployment and Industrial Production in the US. We all know instinctively that sentiment tends to exaggerate the underlying economy due to behavioural biases like recency. This is further exacerbated by the pervasiveness of business television and social media. But the gap appears to be in record territory. Irrational exuberance, anyone?

Of course, these lines can converge into a happy middle. Confident households and emboldened businesses can collectively spur a virtuous circle of greater economic activity through increased consumption and investment. OR… a splash of cold water like another spectacular Congressional debacle, a moronic 3AM tweet or some new intel on the Russia thingy could move sentiment back in line with the reality of the hard data. To us, it seems sensible to tune positions based on the hard data but always be ready to take advantage of the dislocations signalled when there’s a yuuuge gap between the hard data and the soft data.